- Mar 08, 2026

Urban Food Index- March 6th Update

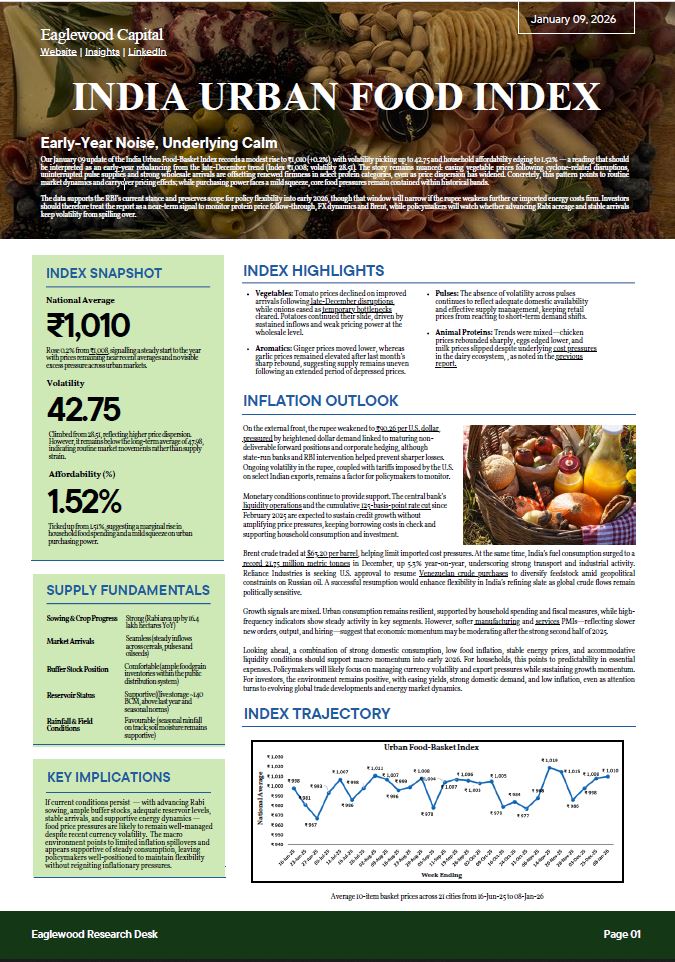

Our March 5 update of the India Urban Food Index shows a sharp decline to ₹880 (-5.3%), the lowest level since the index was introduced, extending the recent correction in food prices. Volatility rose to 55.34 while affordability improved to 1.32%, reflecting the lower cost of the urban food basket. The decline was led by a correction in tomato prices following fresh arrivals since January, alongside softer chicken prices, while ginger prices eased after the previous spike. Chickpea prices moved within a narrow band with a slight festive uptick, while eggs and onions prices showed limited movement across recent readings.Supply conditions remain supportive, with robust rabi sowing, steady market arrivals, adequate buffer stocks and improving reservoir storage reinforcing supply visibility across key staples. The latest configuration suggests food inflation remains comfortable despite higher volatility. Domestic supply fundamentals continue to provide a stabilising cushion even as external risks persist, including geopolitical tensions and currency pressures linked to global energy markets. Monetary policy signals also remain steady, with interest rates expected to stay around current levels as the central bank focuses on liquidity management within the policy corridor while monitoring growth, inflation dynamics and external developments.